Unlocking consumers’ willingness to pay for AI

Aug 06, 2026

By Mutiara Nuralita and Ivan Adi Winata AI users are everywhere, but paid AI users are not Most

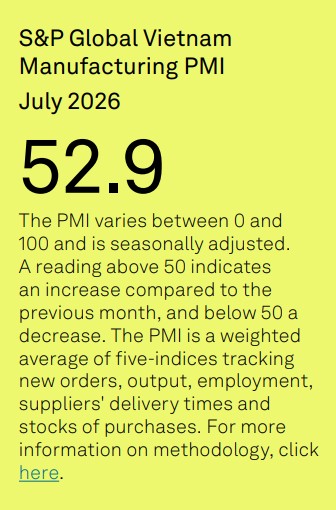

Vietnam PMI July 2026 – manufacturing purchasing managers index

Cimigo Vietnam market research has collected the Vietnam PMI – manufacturing purchasing managers index since 2013. S&P Global compiles the Vietnam PMI S&P Global from responses to monthly questionnaires sent to purchasing managers in a panel of around 400 manufacturers.

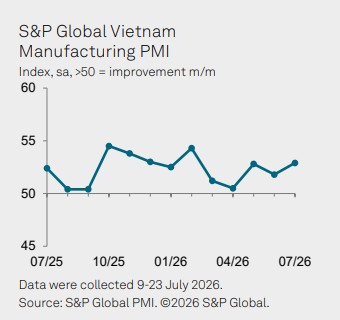

July data pointed to a strengthening of growth momentum in the Vietnamese manufacturing sector. Sharper increases in output, new orders, exports and purchasing were recorded, while employment rose for the first time in five months. Firms were helped by a further easing of inflationary pressures, with input costs and output prices each rising at the slowest rates in 10 months. Supply-chain delays were also less pronounced.

The S&P Global Vietnam Manufacturing Purchasing Managers’ Index™ (PMI®) rose to 52.9 in July, up from 51.8 in June and signalling a solid monthly improvement in the health of the sector. Business conditions have now strengthened in 13 consecutive months, with the latest improvement the most pronounced since February.

Manufacturing production increased sharply in July, with the rate of expansion quickening to a five-month high. Output has now risen continuously on a monthly basis since May 2025. Firms often linked higher output to an increase in new orders. New business expanded for the third month running in July, and at a faster pace than in June. Total new sales were supported by a solid increase in new export orders, which rose at the sharpest rate since July 2024.

Anecdotal evidence indicated that the improving growth picture in the sector was in part reflective of an easing of inflationary pressures. Although respondents continued to report rising prices for shipping, and there were some mentions of further increases in fuel and oil costs, a recent dip in the oil price meant that other firms were able to make savings. As a result, both input costs and output prices increased at the slowest pace since September 2025.

Supply-chain disruption also softened further in July, with suppliers’ delivery times lengthening to the least marked extent since May 2025. Where lead times did increase, panellists linked this to shortages of goods and transportation.

Meanwhile, manufacturers ramped up their purchasing activity in July, with the rate of expansion the steepest in almost four-and-a-half years. According to respondents, the rise in input buying mainly reflected higher output requirements, although some firms purchased items for use in the future.

With inputs being utilised to support sharply rising production, stocks of inputs continued to fall markedly. Stocks of finished goods were also down as products were shipped to customers to help satisfy order requirements. Manufacturers also responded to greater workloads by taking on extra staff, the first time this had been the case in five months. That said, the pace of job creation was insufficient to prevent a build-up of backlogs of work amid solid new order growth.

Hopes that new orders will continue to rise and plans for expanded production capacity were among the factors supporting confidence in the 12-month outlook for output in July. Sentiment rose to a five-month high, but was still some way below the level seen just before the outbreak of war in the Midde East as some panellists highlighted the potential for geopolitical issues to limit growth.

The S&P Global Vietnam Manufacturing PMI® is compiled by S&P Global from responses to monthly questionnaires sent to purchasing managers in a panel of around 400 manufacturers. The panel is stratified by detailed sector and company workforce size, based on contributions to GDP.

Survey responses are collected by Cimigo Vietnam in the second half of each month and indicate the direction of change compared to the previous month. A diffusion index is calculated for each survey variable. The index is the sum of the percentage of ‘higher’ responses and half the percentage of ‘unchanged’ responses.

The indices vary between 0 and 100, with a reading above 50 indicating an overall increase compared to the previous month, and below 50 an overall decrease. The indices are then seasonally adjusted.

Unlocking consumers’ willingness to pay for AI

Aug 06, 2026

By Mutiara Nuralita and Ivan Adi Winata AI users are everywhere, but paid AI users are not Most

The Road to Saigon

Apr 15, 2025

Watch the Road to Saigon and learn about the stories of the residents. Understand their lives,

Vietnam uninterrupted: a twenty-year journey

Mar 18, 2024

Trends in Vietnam: Vietnam uninterrupted: a twenty-year journey Trends in Vietnam. Witness

Đoàn Ngọc Huy (Johnny Doan), CMO & Market Research Expert -

As a Marketing Director and Market Research Expert Advisor across international markets, I have collaborated with numerous market research agencies, both global and local, that operate with a high level of professionalism and effectiveness. Cimigo is among the most outstanding. The Cimigo team demonstrates exceptional professionalism, strong commitment, and operational excellence. From research design and fieldwork execution to insight analysis, all stages are conducted rigorously, delivered on schedule, and closely aligned with business objectives. This is a highly capable team that I would confidently recommend to my partners and stakeholders.

As a Marketing Director and Market Research Expert Advisor across international markets, I have collaborated with numerous market research agencies, both global and local, that operate with a high level of professionalism and effectiveness. Cimigo is among the most outstanding. The Cimigo team demonstrates exceptional professionalism, strong commitment, and operational excellence. From research design and fieldwork execution to insight analysis, all stages are conducted rigorously, delivered on schedule, and closely aligned with business objectives. This is a highly capable team that I would confidently recommend to my partners and stakeholders.

Lisa Nguyen - Vietnam Marketing Lead

Mark Ratcliff - Managing Director

The team at Cimigo are my favourite researchers in South East Asia. They’ve proved adept at tackling the most private and complex personal issues at qualitative research level, not flinching when the client endlessly chopped and changed fieldwork timing, or ramped up the workload without warning. They have recruited the most extraordinarily niche consumers without pause or complaint. Their patience with clients and their flexibility and hard work that went above and beyond what was initially asked of them on two projects relating to sexual behaviour means there is now no other research company we would choose to work with in that part of Asia. The fact they also pulled off a third project for us so well, on men’s relationship with beer and beer advertising, shows they have breadth of expertise— we still quote from the report they produced.

The team at Cimigo are my favourite researchers in South East Asia. They’ve proved adept at tackling the most private and complex personal issues at qualitative research level, not flinching when the client endlessly chopped and changed fieldwork timing, or ramped up the workload without warning. They have recruited the most extraordinarily niche consumers without pause or complaint. Their patience with clients and their flexibility and hard work that went above and beyond what was initially asked of them on two projects relating to sexual behaviour means there is now no other research company we would choose to work with in that part of Asia. The fact they also pulled off a third project for us so well, on men’s relationship with beer and beer advertising, shows they have breadth of expertise— we still quote from the report they produced.

Kevin McQuillan - Chief Marketing Officer

Sam Houston - Chief Executive Officer

Minh Thu - Consumer Market Insights Manager

Travis Mitchell - Executive Director

Malcolm Farmer - Managing Director

Hy Vu - Head of Research Department

Joe Nelson - New Zealand Consulate General

Steve Kretschmer - Executive Director

York Spencer - Global Marketing Director

Laura Baines - Programmes Snr Manager

Mai Trang - Brand Manager of Romano

Hanh Dang - Product Marketing Manager

Luan Nguyen - Market Research Team Leader

Max Lee - Project Manager

Chris Elkin - Founder

Ronald Reagan - Deputy Group Head After Sales & CS Operation

Chad Ovel - Partner

Private English Language Schools - Chief Executive Officer

Rick Reid - Creative Director

Anya Nipper - Project Coordination Director

Dr. Jean-Marcel Guillon - Chief Executive Officer

Joyce - Pricing Manager

Matt Thwaites - Commercial Director

Aashish Kapoor - Head of Marketing

Kelly Vo - Founder & Host

Thanyachat Auttanukune - Board of Management

Hamish Glendinning - Business Lead

Thuy Le - Consumer Insight Manager

Richard Willis - Director

Ha Dinh - Project Lead

Geert Heestermans - Marketing Director

Vo Thi Thuy Ha - Commercial Effectiveness

Louise Knox - Consumer Technical Insights

Aimee Shear - Senior Research Executive

Dennis Kurnia - Head of Consumer Insights

Tania Desela - Senior Product Manager

Thu Phung - CTI Manager

Linda Yeoh - CMI Manager

Cimigo’s market research team in Vietnam and Indonesia love to help you make better choices.

Cimigo provides market research solutions in Vietnam and Indonesia that will help you make better choices.

Cimigo provides a range of consumer marketing trends and market research on market sectors and consumer segments in Vietnam and Indonesia.

Cimigo provides a range of free market research reports on market sectors and consumer segments in Vietnam and Indonesia.